Today’s crises are not sudden; they are the slow release of tensions accumulated since the 1970s pivot from production to finance.

What if the acceleration we feel today is not a product of screens and polarization but the much delayed, slow-release (like healthy carbs) consequences of a structural transformation that began decades ago?

In the 1970s, when the postwar reconstruction boom ended after an oil shock that started amid a turmoil similar to today’s Middle East mess, advanced economies pivoted from production to financialization. Though the story could have been much different.

The 1970s were not simply a decade of crisis. They were a crossroads: faced with the end of the postwar reconstruction boom, advanced economies could either reinvent the productive economy or pivot toward financialization and globalization. The world chose the latter, which was the easiest path for capital. This also happened to be the most traumatic for those depending on industrial jobs.

The stagflation that changed society and politics forever

For half a century, globalization, credit expansion, and financial markets postponed the consequences of a deep crisis that began with expensive energy, high inflation, and low consumer confidence.

But, underneath the growth and prosperity at the top, a long-term decline in manufacturing and heavy industry in advanced economies affected millions of workers who didn’t transition to services and the knowledge economy. To many people, trouble didn’t start a few months ago or even a few years back; to them, it’s already a generational problem that feeds today’s politics of resentment.

French historian Fernand Braudel argued that the events that we perceive as sudden, spontaneous crises are mere happenings on the surface. In reality, says Braudel, the real causes are always slow structural changes that accumulate over years, decades, or even centuries.

Another way to see it: European countries can’t rely on their own fossil fuel production and reserves, which are nonexistent, and so their real obsession should be to structurally guarantee their energy self-reliance through other means of energy production, from renewables to nuclear.

You say single event, I say underlying causes

Following Braudel’s thinking, our obsession with capturing what’s happening at every instant prevents us from seeing the story evolving over time. Current underlying turbulences—geopolitical, economic, and political—may therefore represent not a sudden rupture but the long-delayed release of tensions accumulated since the end of the postwar economic miracle.

Perhaps we could start with a story that goes back deeper in time, much like Peter Frankopan’s The Silk Roads: perhaps, the real center of global history has been the Silk Roads region all along, from pre-Biblical times to today.

As if we were haunted by some sort of Jungian collective unconscious, we always go back to Persia, Mesopotamia, the Levant, Central Asia, and Anatolia. Merchants, empires, religions, armies. In Frankopan’s interpretation, oil is essentially the modern equivalent of silk and other precious commodities from the past (spices, metals, horses, textiles).

Ancient chokepoints incentivized European kingdoms to seek other routes in the Age of Discovery, but so far, modern oil chokepoints (like today’s strategic Strait of Hormuz) have barely switched the world’s dependence, only relativized it: renewables and shale oil in North America have reduced dependency but not erased it.

The mess in the Middle East right now is a reminder that some of the stressors that accelerated that shift are still at the table, influencing how we live and might live in the future, and preventing us from once and for all seeking alternatives to it.

A short-attention-span world

Just a few years back, when things were beginning to REALLY accelerate from the agenda-setting perspective, some weeks felt like years, packed to the rim with important events that, in isolation, would have required months of single-handed attention mere years back.

Then came the first Trump administration, and spin doctoring became a lucrative full-time job for many, and some days packed into one DAY began to feel like years of information and controversy.

Fast-forward eight years, and Trump’s second term is the confirmation that things aren’t slowing down, and the only way to maintain a precarious equilibrium between remaining on the loop of essential information and personal sanity is, well, up to any of us, for no guardrails (old or new) will return our world to a boring, predictable, stable, slow-news era.

That said, if we forget for a moment the permanent smokescreen deployed by the United States lately, little has changed in geopolitics; we can simply see things now in the open, in their full, raw rudeness. In today’s tacky international politics, old-school diplomacy feels as out of place as powdered wigs at a Jacobin rally: the more refined your manners, the quicker you risk losing your head, as you’ll be perceived as weak.

However, we shouldn’t be too quick to catastrophize, and many believe that a big-picture perspective is needed to put things in their proper place. The tensions that dominate today’s most pressing issues have long been in the making, and any kind of action (yes, even chaos and improvisation, which is what we’re seeing) will at least help free advanced societies from the sclerosis and relative decay that have been plaguing them.

When reconstruction prosperity stopped in the 1970s

One of the most important theses from Thomas Piketty’s controversial book Capital in the Twenty-First Century isn’t his take that long periods of prosperity will make the rich richer and the middle class pay more taxes while becoming relatively poorer, but the fact that he acknowledges that, given the inability of prosperous societies to redistribute wealth in the last decades, there’s only one main old-school way so make societies more dynamic: big systemic shocks like big, painful wars.

Piketty isn’t inventing this; he just proves that the two world wars did precisely this, and the prosperity created in North America, Europe, and Japan was a consequence of the painful tabula rasa that killed millions of people and obliterated entire cities and industries. If no stressors are introduced (e.g., a major war that requires reconstruction across the board, or significant wealth-redistribution policies), inequality tends to grow over time in fairly open capitalist societies.

So, according to Piketty’s take, if no shock is inflicted, over time, the rate of return on capital “r” (profits, dividends, rents, interest) will grow much faster than real economic growth “g” (income, output). Or r > g. But Piketty’s book, written before the pandemic, doesn’t explain why after the last big economic shocks, from the subprime and sovereign debt crisis to Covid-19, return on capital “r” rebounded more energetic than ever and the “real economy” (debt added, and taxes, direct and indirect, that mainly the middle class will pay) is the one struggling to get by.

After World War Two, many European countries and Japan benefited not only from the Marshall Plan but also from the ability to start over with cheap credit and a wealth of opportunities, and the decades that followed the shock were called a “miracle” for some reason. A majority of Western countries and Japan experienced post-war booms so strong that those years were given grandiose names like Il Miracolo (Italy), Les Trente Glorieuses (France), Wirtschaftswunder (“economic miracle,” West Germany), and the working and middle classes experienced a remarkable rise in prosperity.

Interestingly, it was never the mirage of trickle-down economics that created prosperity across the board and raised generational wealth among the middle class, but a unique set of conditions in Europe and Japan (like the massive rebuilding needed after the war, as well as demand for steel, cement, machinery, consumer goods, etc.), as well as the United States’ intact industrial output which turned into exports of machinery, cars, chemicals, consumer goods, and a dominant cultural industry.

Then came the 1970s, and the postwar Golden Age began to falter. There’s no single culprit that explains the loss of dynamism in advanced economies as they hit the 1970s, but many of the factors that began eroding the middle class and generating the inequality gap now experienced in the US sound familiar half a century later, reminding us that history rhymes, if not more.

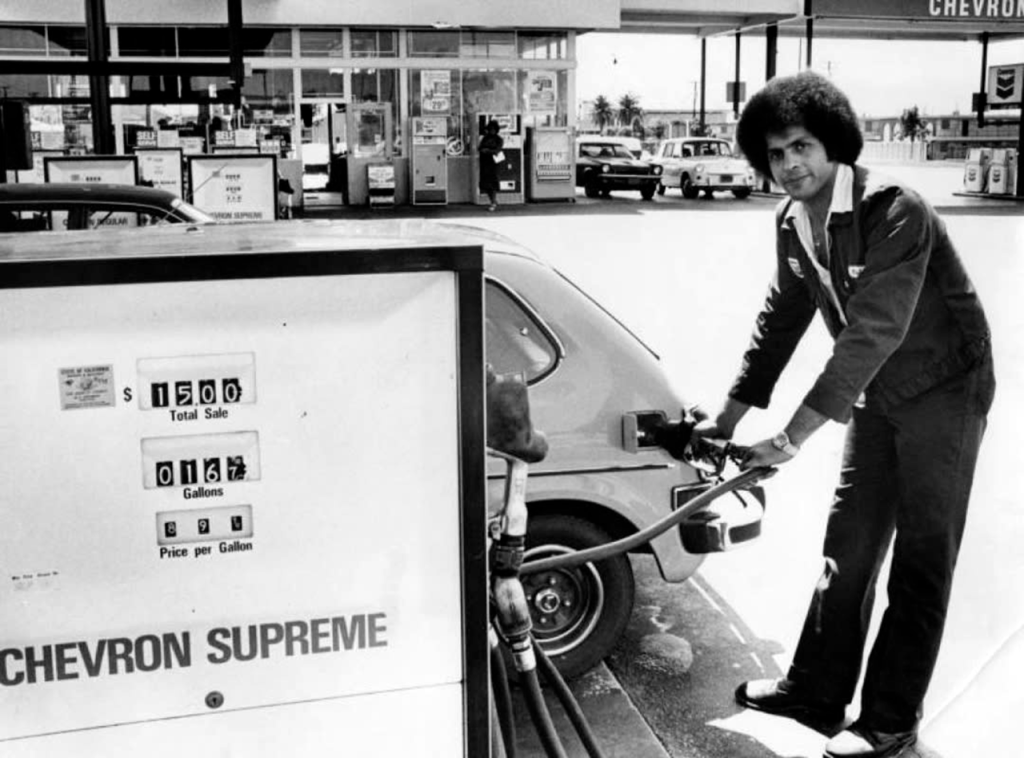

Waiting at the pump in the 1970s vs. tomorrow

Amid the difficult equilibrium of the Cold War and the Middle East, which grew shakier after the Yom Kippur War, leading to the 1973 oil shock once OPEC imposed an oil embargo on Western countries, leading to a double-edged crisis of low growth and high inflation. And so, with stagflation, the prosperity engine created after World War Two mainly stopped working.

As growth based on reconstruction ended and currencies began floating after the collapse of the fixed-currency monetary order (established at Bretton Woods, financial volatility followed, and so real “reconstruction” and industrial innovation (cars, steel, concrete, appliances, planes) faltered in favor of financial speculation. In parallel, rising labor costs and rigid labor markets were the excuse corporations used to team with new Administrations in favor of deregulation. The tide of offshoring had started and wouldn’t be stopped.

Where do we fit, people often born after the 1973 oil embargo, in this macro picture? We’re late on the picture, but entered it right in time to assist in our lifetimes to the acceleration of this shock, once China, which had been left out the postwar boom of 1949-1976, approved Deng Xiaoping’s 1978 reforms to open to foreign investment and, more importantly, create Special Economic Zones (SEZs) that—as Shenzhen would show soon enough—would become the actual factory of the world.

Perhaps many of our ills today go back to the early 1970s, when the “economic miracle” of productive economies that were, at once, “reconstructing” the world and fostering a prosperous middle class stopped working, helped by the shock of stagflation. Millions of jobs would be lost, and countries were about to increase borrowing to artificially keep prosperity on par with rising prices.

When public spending to stimulate the economy stopped working, the new liberal paradigm represented by Ronald Reagan and Margaret Thatcher created a different type of growth that economists like Tyler Cowen have associated with the phenomenon of the “great stagnation“: without big ideas of “reconstruction,” deregulated markets and fewer taxes favored a different type of investment and growth, creating an economy less productive and more interested in returns to capital (housing) and financial investment. Other economists and historians have advanced a similar narrative, including Branko Milanović, Adam Tooze, and Wolfgang Streeck.

The real losers of the 1970s never recovered

When we talk about the financialization of advanced economies after the 1970s, it’s not an abstract idea. As real profits and big investments shifted from “production” of stuff to “assets,” a large part of the middle class began to suffer phenomena like salaries barely keeping up with inflation and the fear of offshoring, while financial profits and real estate speculation drove prosperity among the asset class. Like it could happen in the coming years with AI, the rug was pulled under them, with nowhere to hide or feel protected from the shock.

And so, one of the great swindles in modern economic history managed to deplete industries, impoverish the middle class over time, and profoundly reshape incentives in the economy, making countries less industrial and more financial as wealthy people and entities allocated their main investments into assets that had little to do with the productive economy. Real Estate and financial fortunes were made, and investors like Buffett and Munger became the new heroes of get-rich-quick self-help literature.

Perhaps we can attribute many of today’s ills to the convoluted 1970s, when many of us were born. Those were years of Middle East entanglement and a world of geopolitics turning on the price of a single commodity: oil. Same issues, same culprits, same landscape fifty years later, only now we can prompt AI to make memes about it.

European powers are as vulnerable to the shock as they were half a century ago and are poised to pay the lingering consequences of the current conflict this time, too. One thing has changed: the US is now the world’s largest oil producer and is less affected by energy prices and supply contingencies.

Interestingly, the tumult of the 1970s also brought forth proposals from people who didn’t want to resign themselves to a world defined by macro-history and wanted to give agency and the tools of prosperity back to individuals. The 1970s oil crisis sparked debates about alternative ways to keep a productive economy, rather than closing factories and letting markets (with the help of deregulation) decide which models would survive.

Many things weren’t inevitable as we’ve been told. Decisions were made to close entire profitable, cutting-edge factories to produce more cheaply elsewhere, for example. If many framed this moment as economic Darwinism, the economic output leading to Reaganomics was created by a series of decisions: some priorities won, and some—like investing in cutting-edge renewable energy, as well as the promotion of employer-owned factories much in the fashion of the Basque cooperative conglomerate Mondragón—were buried for decades to come.

Economics as if people mattered. LOL

During the early 1970s, in a matter of 3-4 years, several influential books made it to the public debate, universities, and the desks of the growing—if impoverished—creative classes: Ivan Illich published Deschooling Society (1971) and Tools for Conviviality in 1973, the year of the OPEC shock and another remarkable book publication, E.F. Schumacher‘s Small is Beautiful: Small Is Beautiful: Economics as if People Mattered.

None of these books addresses the problems of their time from a closed, formulaic point of view, but they start with a shared perspective: industrial society had grown too large and centralized, and so it had become too dependent on externalities that individuals could not control, from the manipulation of labor movements to politization and corporatism, to off-shoring.

Hence, the proposal to preserve prosperity by preserving a productive economy could not come from a model that had stopped working once the postwar boom ended. Through their books, authors like Illich and Schumacher proposed new ways to create productive jobs locally. Instead of doubling down on financialization, deregulation, and globalization, they explained how, in practice, human-scale technology could actually work and bring local autonomy. Illich even talked about “convivial” tools capable of “augmenting” people’s potential, much as personal computing pioneers were developing. People could really do more with less while staying productive and unleashing their inventiveness. Economies, in turn, could work in a decentralized way.

If their ideas sound very much like the concepts that inspired the Xerox PARC in Palo Alto and visitors to it like Steve Jobs, it’s not a coincidence: the 1970s didn’t just produce two economic paradigms (Reaganomics and the ideals of human augmentation to proper tools that empower instead of enslaving people, a bit like Ridley Scott’s original ad for the Macintosh in 1984), but also two technological philosophies.

On the one hand, the 1970s produced Illich, Schumacher, the Whole Earth Catalog, and the concept of ecological economics, but this idealization also inspired real-world advances such as organic agriculture, personal and networked computing, and the world of human-centered interfaces we live in today.

In the macro world, however, the world took the path of financialization, globalization, and neoliberalism, and offshoring accelerated the despair in hollowed-out cities and old suburbs, as society as a whole seemed to prosper at a faster rate than ever before. This picture, however, had forgotten about the productive economy or how the middle class had to reinvent itself.

From oil chokepoints to AI chokepoints

Not all hippies turned into yuppies, and not all yuppies turned into tech bro investors, but the evolution of personal computing and the internet from the days of young John Perry Barlow to today’s digital world is a tale of hits and misses, and how potentially “convivial” and “democratizing” tools can be weaponized to evolve into their Matrix-like antagonists. To Illich, the printing press had been convivial and had empowered individuals like no other tool before in our era, and other tools like

bicycles, hand tools, and small-scale workshops showed how to give power back to users rather than requiring experts or bureaucracies to “codify” it.

Back in the seventies, authors like Illich and Schumacher were influencing the very people who were developing personal computing, many of whom were wary of what they called “radical monopolies” (when industrial systems eliminated alternatives). If cars dominated cities completely, they would turn into something different, and walking would become impossible. The same happened with tools as they grew to gigantic scale, to the point that they created the opposite of their intended purpose.

Brought to an extreme, Illich thought, when radical monopoly systems become entangled in societies, they stop offering an optional service, forcing people to depend on it. Pushed to the extreme—he argued—valuable industrial tools turned out to be counterproductive for people because they produced the opposite of their intended purpose.

For example, if schooling turns out to be, first and foremost, a business of teaching people how to make money, it may be suppressing genuine learning (is this the evolution of higher education?). And how about smartphones or tech platforms that started offering a very useful service before they began capturing much more value than what they give back to people in return?

To prevent institutions, companies, and services from creating too much value and obliterating people’s autonomy and agency, Ivan Illich thought that tools needed to develop a “convivial” rather than dominating finality. His point of view is prescient once again, as we shift from the strategic wars of yesterday (oil in the Middle East) to the battle for control of rare earths, advanced chips and energy needed to power the data centers of AI.

Today’s Faustian bargain

Oil was central as a key input for modern industry (transportation, manufacturing, power generation, logistics), whereas AI is turning out to be what will power automation, scientific discovery, new manufacturing, robotics, military decision systems (as we already see in the news), and frontier discovery in any field we can imagine.

As AI becomes embedded across industries and functions like an infrastructure layer we cannot detach from basic everyday actions, how can we make sure, as autonomous individuals and as societies, that we follow the advice of Ivan Illich and demand a “convivial” companion that augments our capacities instead of turning us into a battery to power its own ultimate purpose?

So far, things aren’t looking promising if, as Josh Dzieza explains, highly valuable people on their fields of expertise who struggle to find a job are deciding to make the ultimate Faustian bargain: by providing their masterful responses to AI patterns and prompts, they’re helping LLMs to get better at more and more skills, ultimately training models to take over their work:

“Daron Acemoglu, a professor of economics at MIT who studies automation, compares the situation to that of weavers, who before the industrial revolution were “like the labor aristocracy,” self-employed artisans in control of their own time. Then came weaving machines, and in order to survive, they were forced to take new jobs in factories, where they worked longer hours for less money under the close supervision of management. The problem wasn’t simply that technology took their jobs; it enabled a new organization of work that gave all power to the owners of capital, who made work a nightmare until labor organizing and regulation set limits.”

Can AI be convivial? Regulation won’t help us make it so

The question raised by Ivan Illich is now more urgent than ever: if AI becomes a centralized, highly controlled infrastructure, who can rein in such a radical monopoly capable of reducing human agency to the margins?

At the same time, one supervised AI that learns to be convivial could be the most valuable tool ever invented, a cognitive companion that augments people’s potential and expands creativity.

Perhaps the fork in the road that appeared in the 1970s may not have been discarded, after all, but simply postponed half a century.

Will our tools empower us, or will we reorganize society to serve them, entering The Matrix?